Medicare enrollment periods can feel complicated, yet they follow specific rules that determine when you can sign up for coverage. Missing deadlines can lead to penalties, gaps in coverage, or higher costs, so understanding these periods is essential. Each enrollment window serves a different purpose, and knowing how they work ensures that you make informed decisions about your healthcare.

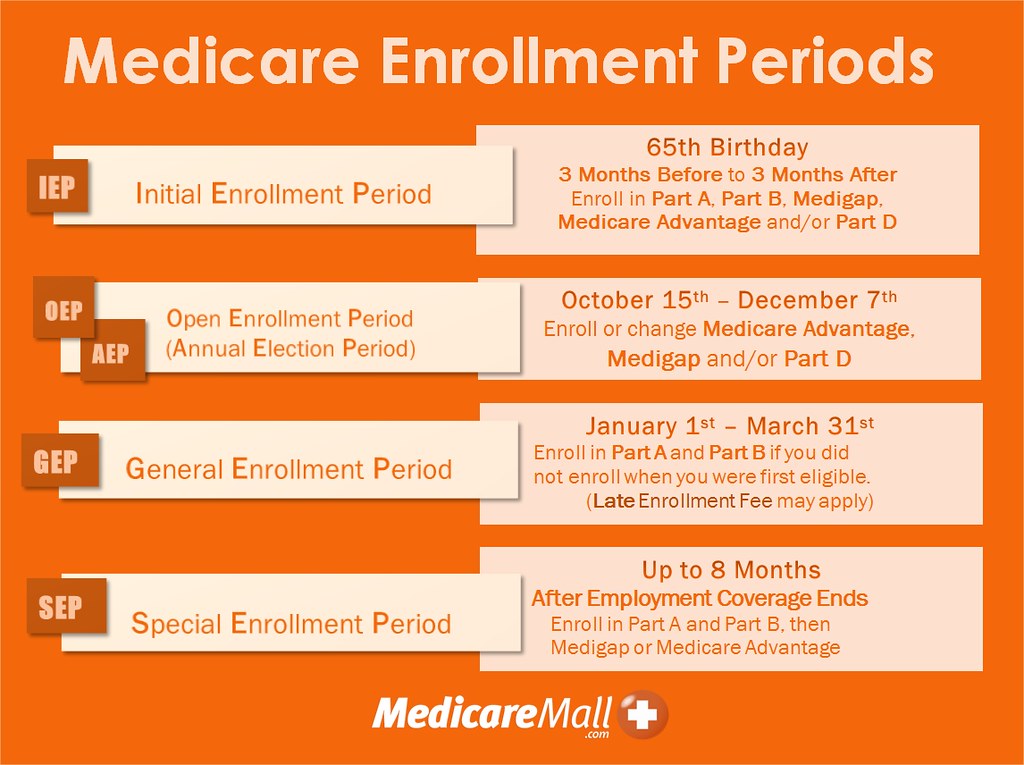

Initial Enrollment Period (IEP)

The Initial Enrollment Period is the first chance to sign up for Medicare. It begins three months before the month you turn 65, includes your birthday month, and continues for three months afterward. In total, you have seven months to enroll.

During this time, you can sign up for Medicare Part A, which covers hospital services, and Part B, which covers outpatient care. If you want prescription drug coverage, you can also enroll in Part D. Many people choose Medicare Advantage, also known as Part C, which combines Parts A and B with additional benefits.

Coverage start dates depend on when you enroll. Signing up before your birthday month ensures coverage begins promptly, while waiting until later in the window may delay the start date. Missing this period often results in late enrollment penalties, especially for Part B and Part D.

General Enrollment Period (GEP)

The General Enrollment Period provides another chance if you missed your Initial Enrollment Period. It runs every year from January 1 through March 31, with coverage beginning on July 1 of the same year.

During this time, you can enroll in Part A and Part B, but penalties may apply. For Part B, the penalty is an increase in your monthly premium, lasting as long as you have coverage. For Part D, penalties apply if you go without prescription drug coverage for more than 63 days.

The General Enrollment Period ensures that people who missed their first opportunity can still enroll, but waiting until this time may leave you without coverage for several months.

Special Enrollment Periods (SEPs)

Special Enrollment Periods allow you to enroll outside of the Initial or General Enrollment windows under certain circumstances. Common examples include continuing to work past age 65 and having employer‑sponsored health coverage. When that coverage ends, you qualify for a Special Enrollment Period.

Other situations include moving to a new area, losing other insurance, or qualifying for Medicaid. Special Enrollment Periods vary in length, but most last eight months after employer coverage ends. Enrolling during a Special Enrollment Period helps you avoid penalties and ensures continuous coverage.

Coverage Start Dates

Coverage start dates depend on the enrollment period. During the Initial Enrollment Period, enrolling early ensures coverage begins the month you turn 65. Enrolling later may delay coverage by one to three months.

During the General Enrollment Period, coverage always begins on July 1. Special Enrollment Periods vary, but coverage usually starts the month after you enroll. Understanding these timelines helps you plan for medical needs and avoid gaps in coverage.

Penalties for Late Enrollment

Late enrollment penalties can be costly and long‑lasting. For Part B, the penalty is 10 percent of the premium for each 12‑month period you delayed enrollment. For Part D, the penalty is 1 percent of the national base premium for each month you went without coverage.

These penalties last as long as you have coverage, making them a permanent financial burden. Avoiding penalties requires enrolling during your Initial or Special Enrollment Period.

Automatic Enrollment

Some people are enrolled automatically. If you receive Social Security benefits at least four months before turning 65, you are automatically signed up for Medicare Parts A and B. Coverage begins the first day of your birthday month, or the month before if your birthday falls on the first day of the month.

Automatic enrollment ensures that you do not miss deadlines, but you should still review your options. You may want to add Part D or choose Medicare Advantage. Reviewing automatic enrollment ensures that your coverage matches your health and financial needs.

Professional Guidance

Medicare rules can feel complex, especially when balancing work coverage, retirement, and medical needs. Seeking guidance from licensed agents, State Health Insurance Assistance Program (SHIP) counselors, or financial advisors helps you understand enrollment periods clearly. Professionals explain rules, compare plans, and help you avoid penalties.

Guidance ensures that you make informed decisions. It also provides confidence that your coverage matches your health and financial goals.

Conclusion

Medicare enrollment periods are designed to give people multiple opportunities to sign up. The Initial Enrollment Period provides the first chance, the General Enrollment Period offers a backup, and Special Enrollment Periods cover unique circumstances. Coverage start dates and penalties depend on when you enroll. Automatic enrollment simplifies the process for some, but reviewing options remains important.

Understanding these rules ensures that you avoid penalties, maintain continuous coverage, and protect your health. Medicare is a vital program, and enrolling at the right time ensures that you receive the benefits you deserve.

Leave a Reply